💰⚖️Most people grind their way through decades of work, scraping into a private pension with the faint hope it might just about keep them warm in their twilight years. Every wobble in the stock market, every fee shaved off by a manager in a shiny office, eats into that pot. And the explanation is always the same: “That’s just how it is. You take the risk, you carry the reward.”

But here’s the dirty little secret: while you’re gambling with your future, you’re also bankrolling someone else’s gold-plated retirement.

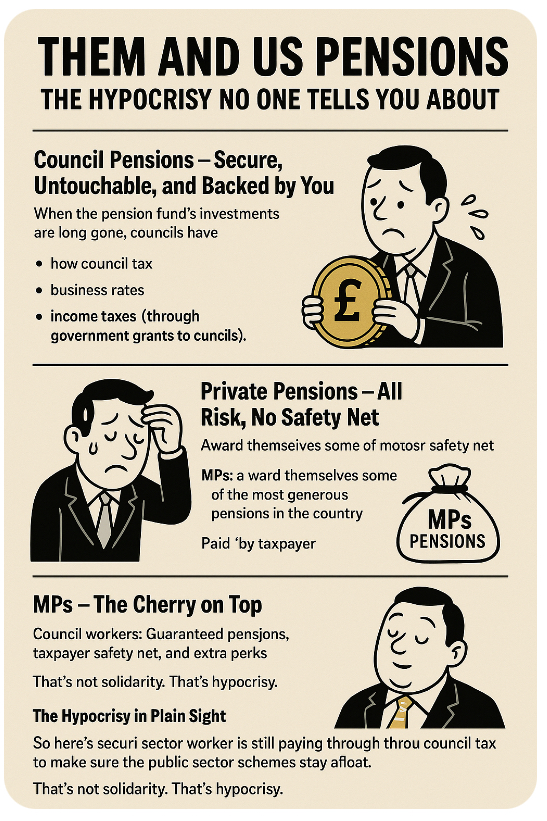

🏛️ Council Pensions: Secure, Untouchable, and Backed by… You

Council workers sit on the Local Government Pension Scheme (LGPS), one of the few old-school defined benefit pensions left standing in the UK. Translation? Their pension is guaranteed for life, based on salary and service, not the roulette wheel of the stock market.

Sounds like a dream, right? A retirement income that doesn’t vanish when Wall Street sneezes. But here’s the catch: when investments don’t quite fill the pot, councils have to top it up. And where does that money come from? That’s right:

- Your council tax 🏠

- Your business rates 💼

- Your income taxes (via government grants) 💷

So even if your own pension pot looks like a kiddie’s piggy bank, you’re still subsidising the bulletproof pensions of local government workers.

🎲 Private Pensions: All Risk, No Safety Net

Meanwhile, in the private sector jungle, the story couldn’t be more brutal. Defined benefit pensions are as extinct as the dodo. What you’ve got now is a pot of hope and despair that relies on:

- how much you can spare each month,

- how kindly or cruelly the markets behave,

- and how much the fund managers siphon off in fees while calling it “stewardship.”

There’s no guarantee, no bailout, no kindly taxpayer sweeping in to save the day. If the market tanks, your retirement tanks with it. Congratulations, you are the safety net.

🍒 MPs: The Cherry on Top of Hypocrisy

And then there’s the Westminster crowd. MPs, those tireless champions of “tightening belts” and “living within our means,” just happen to have awarded themselves some of the most generous pensions in the country. And guess who funds them? Yes, once again: you.

While they tell you to “plan better” and “take personal responsibility,” they sleep soundly on pensions so cushy they could snooze through an economic apocalypse without losing a wink. Crisis? What crisis? Their retirement is bulletproof.

👀 The Hypocrisy in Plain Sight

Let’s spell it out:

- Council workers: Guaranteed pensions, taxpayer top-up.

- MPs: Guaranteed pensions, taxpayer top-up, plus perks on perks.

- Private workers: Market roulette, full risk, zero safety net.

And yet the private worker still chips in — through council tax and income tax — to make sure the public sector schemes never sink. That’s not solidarity. That’s daylight hypocrisy dressed up as “fairness.”

🚨 The Final Word

If pensions are supposed to be secure, then secure them for everyone. If risk is the name of the game, then let the politicians and council chiefs ante up too. Right now, Britain runs on a two-tier pension system: one for them, one for us.

And spoiler alert: you’re paying for both. 🧾

🔥 Challenges 🔥

Are you furious yet? Or just exhausted from being the taxpayer mule pulling two carts — your fragile pension and someone else’s golden one? Let us know: should pensions be levelled out? Or should the “public servants” finally taste the same risks they preach about? Drop your fury, sarcasm, or survival tips in the comments. 💬💥

👇 Comment, like, and share this post — let’s drag this hypocrisy out into the daylight.

The sharpest comments will be featured in our magazine. 📝✨

Leave a comment