🏠🚫💸

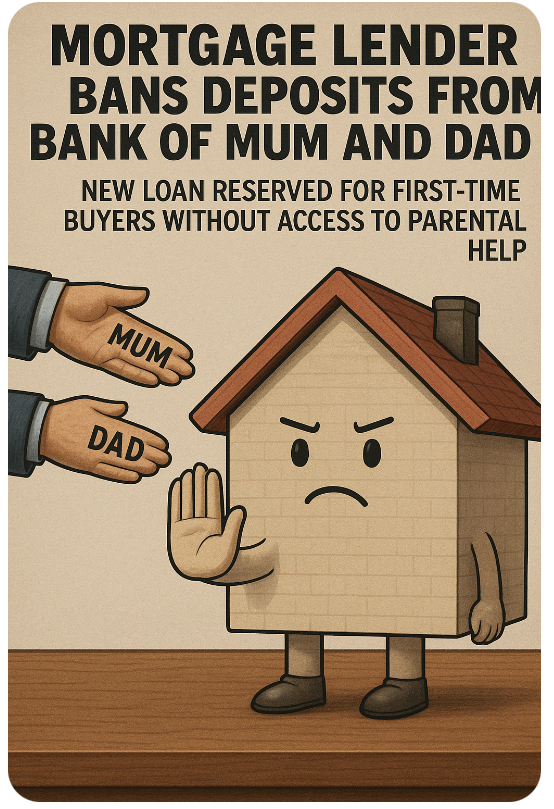

In a plot twist no one asked for, a mortgage lender has decided to ban deposits from the so-called Bank of Mum and Dad. Their shiny new loan is reserved exclusively for first-time buyers who don’t have parental cash propping them up. Sounds noble, right? Except in today’s housing market, buying without family money is about as realistic as finding a unicorn with a credit score. 🦄📉

💰 The Dream Home Hunger Games

Here’s the pitch: finally, a chance for hardworking young people to buy without being outbid by rich kids armed with inheritance cheques and “gifted deposits.” The reality? Those same hardworking young people are already drowning in rent, bills, and overpriced meal deals. Unless you’ve been secretly hoarding Bitcoin or living rent-free in a shed, the idea of scraping together a deposit without family help is laughable.

Meanwhile, the system still rewards landlords, developers, and anyone who’s been playing Monopoly since Thatcher. This new scheme might help a tiny fraction of buyers, but for most, it’s like being offered a lifeboat with a hole in it. Sure, it floats for a bit—but not long enough to stop you sinking. 🚢💦

In truth, the Bank of Mum and Dad isn’t the enemy—it’s the housing system itself, where wages stagnate while house prices rocket like Elon Musk’s vanity projects. If this loan was a sitcom, it’d be called: “Who Wants a Mortgage Anyway?”

🔥 Challenges 🔥

Do you think banning parental deposits levels the playing field—or just sets the bar even further out of reach? Should the focus be on wages, house prices, or kicking landlords into orbit? 🚀💬

👇 Drop your verdict in the comments, like, and share.

The most savage rants and sharpest takes will be featured in the next issue of the magazine. 📝🔥

Leave a comment