For years, investors were told private credit was the smart money’s playground.

Higher returns.

Less volatility.

Sophisticated investments.

What could possibly go wrong? 💰📈

Well, now one of the biggest names on Wall Street has investors asking some uncomfortable questions.

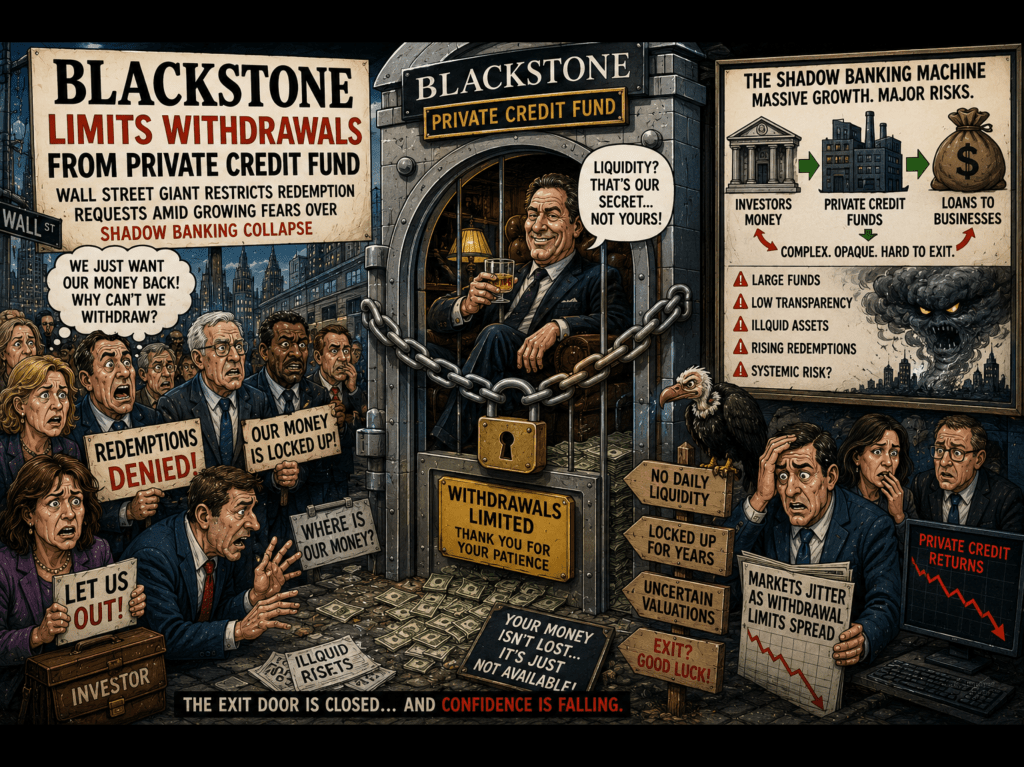

Blackstone has reportedly limited withdrawal requests from one of its private credit funds, a move that immediately reignited fears about liquidity, hidden risks, and whether the booming world of “shadow banking” is starting to show cracks.

Because nothing says “your money is perfectly safe” quite like being told you can’t have it back right now. 🚪🔒

🏦 The Financial Hotel California 🏦

Private credit has exploded in popularity over the last decade.

Traditional banks pulled back from certain types of lending.

Private investment firms stepped in.

Investors piled billions into funds chasing attractive returns.

Everyone celebrated.

Until people started wanting their money back.

That’s where things become awkward.

Unlike cash in a bank account, many private credit investments aren’t easy to sell quickly.

The money is tied up in loans, businesses and complex financial arrangements.

Which means when lots of investors head for the exit at once, the exit suddenly becomes very small.

📉 The Shadow Banking Monster 📉

The term “shadow banking” sounds like something from a Hollywood thriller.

In reality, it refers to financial activity taking place outside traditional banking structures.

Supporters argue it provides valuable funding to businesses.

Critics warn it creates risks that regulators struggle to monitor.

And every time a major fund restricts withdrawals, those warnings get louder.

Because the nightmare scenario is simple.

Investors panic.

Withdrawals increase.

Assets become difficult to sell.

Confidence evaporates.

And suddenly everyone discovers that liquidity is a wonderful thing—right up until it disappears.

🎭 It’s Fine… Until It Isn’t 🎭

Financial markets have a long history of insisting everything is under control.

Right before discovering it isn’t.

From banking crashes to property bubbles, the warning signs often look remarkably similar.

“We have strong fundamentals.”

“Everything remains stable.”

“There is no cause for concern.”

Then someone quietly locks the withdrawal door.

That tends to concentrate minds.

To be fair, withdrawal limits don’t automatically mean disaster.

Many funds have these mechanisms specifically to prevent panic-driven runs.

But investors are increasingly asking whether the private credit boom has become too large, too opaque and too interconnected.

💣 The Question Nobody Wants To Ask 💣

If private credit continues growing while regulation struggles to keep pace, what happens when the next major financial shock arrives?

Will these funds prove resilient?

Or are we watching the early warning signs of a much bigger problem lurking beneath the surface?

That’s the question keeping investors awake at night.

🔥 Challenges 🔥

Do you think private credit is a smart investment opportunity?

Or does the growth of shadow banking pose a serious threat to financial stability?

Should regulators step in more aggressively?

Or are investors simply taking risks they should already understand?

💬 Tell us what you think in the blog comments.

👍 Like the article.

🔄 Share it with friends and fellow investors.

The best comments will be featured in the next issue of the magazine. 📰🔥

Leave a comment